Another Great Article From: Keeping Current Matters Fannie Mae recently released their “What do consumers know about the Mortgage Qualification Criteria?” Study. The study revealed that Americans are misinformed about what is required to qualify for a mortgage when purchasing a home. Here are three takeaways:

- 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO score is necessary

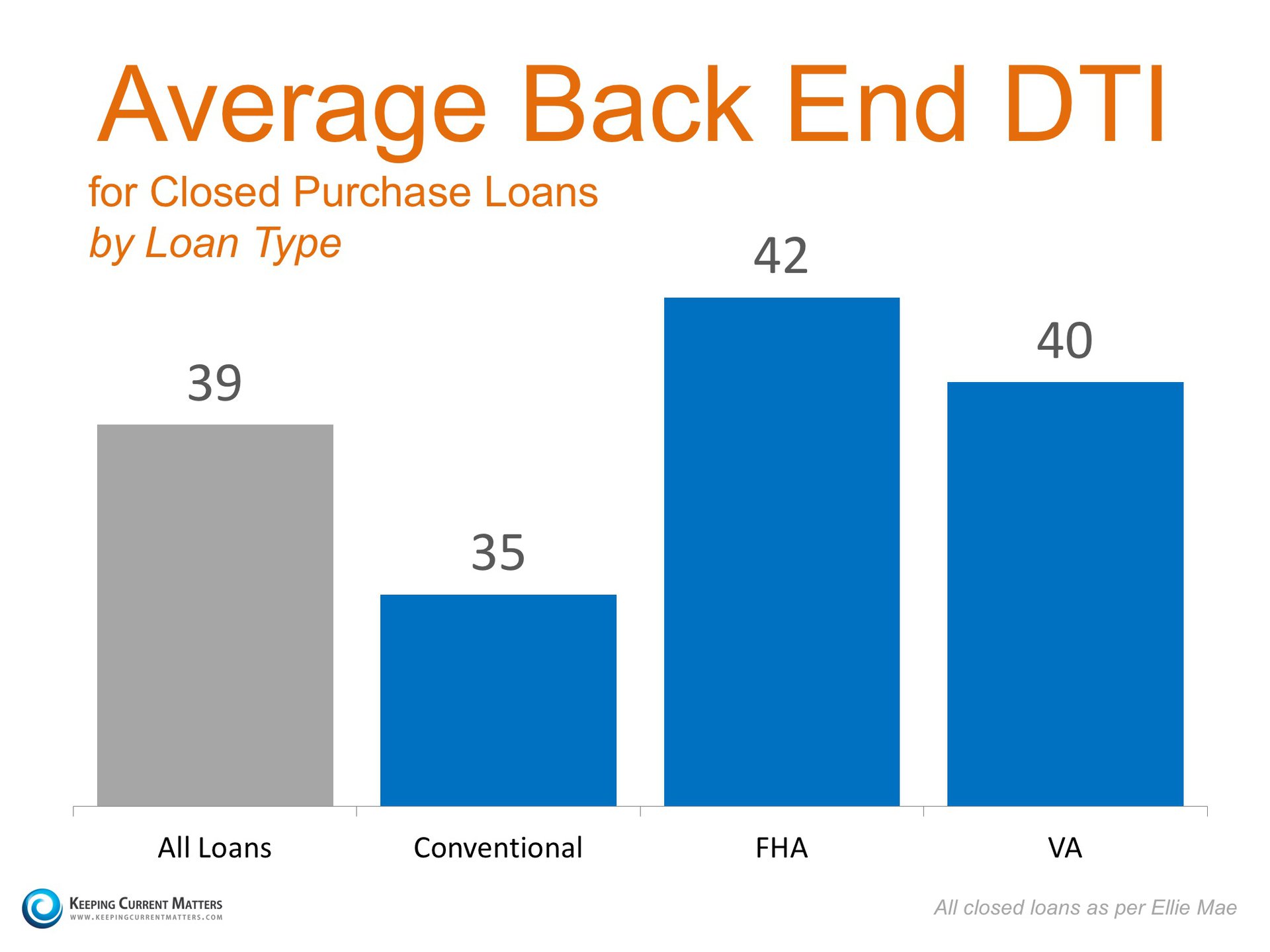

- 86% of Americans either don’t know (59%) or are misinformed (25%) about what an appropriate Back End Debt-to-Income (DTI) ratios is

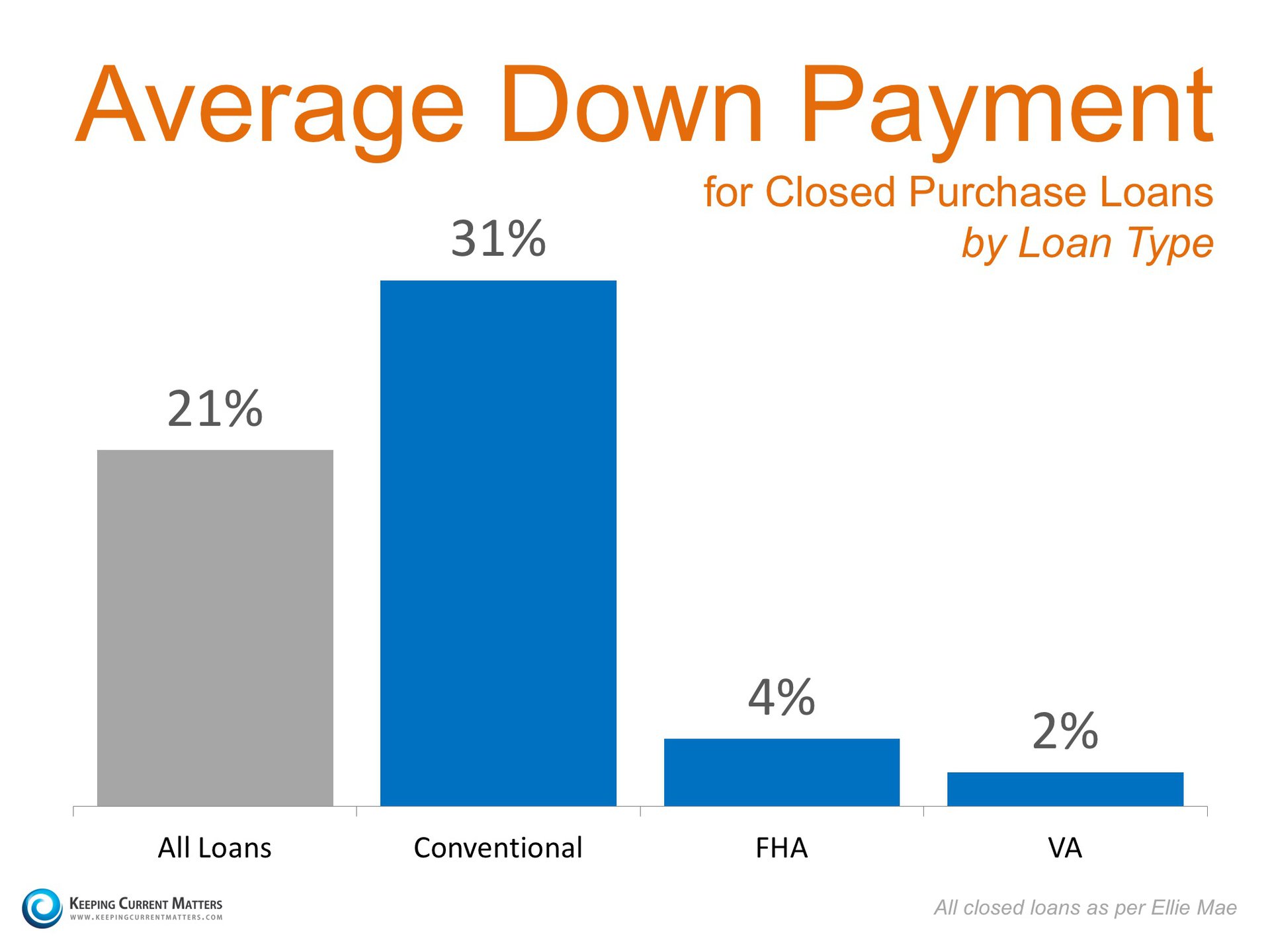

- 76% of Americans either don’t know (40%) or are misinformed (36%) about the minimum down payment required

To help correct these misunderstandings, let’s take a look at the latest Ellie Mae Origination Insight Report, which focuses on recently closed (approved) loans.

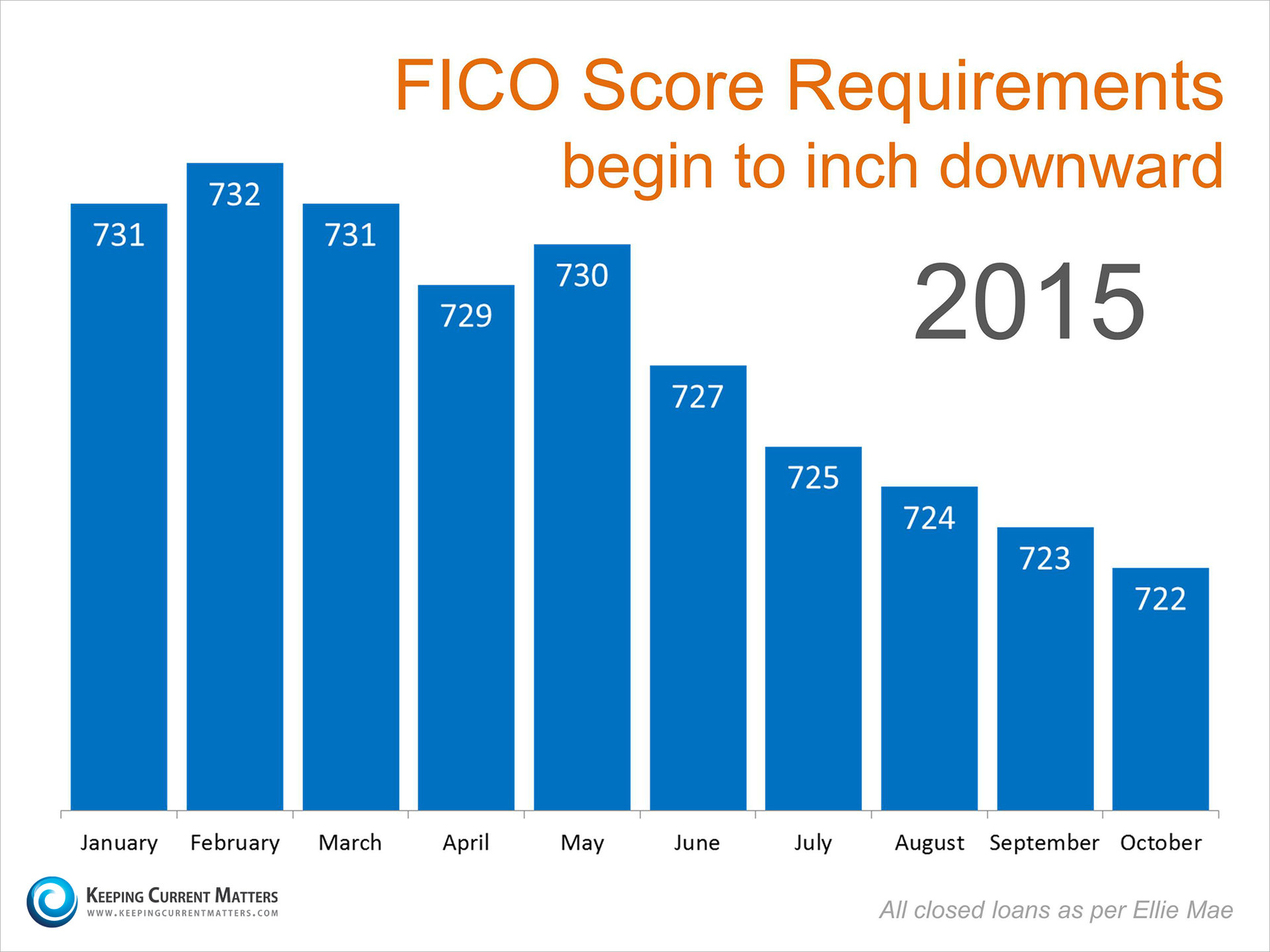

FICO SCORES

BACK END DTI

DOWN PAYMENTS

Bottom Line

Whether buying your first home or moving up to your dream home, knowing your options will definitely make the mortgage process easier. Your dream home may already be within your reach.

Loan Process

Buy Now or Wait Until 2017

![Should I Buy Now Or Wait Until Next Year? [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2016/01/Cost-of-Waiting-KCM.jpg)

Some Highlights:

|

Share this:

Nine Steps To Buying A Home

Share this:

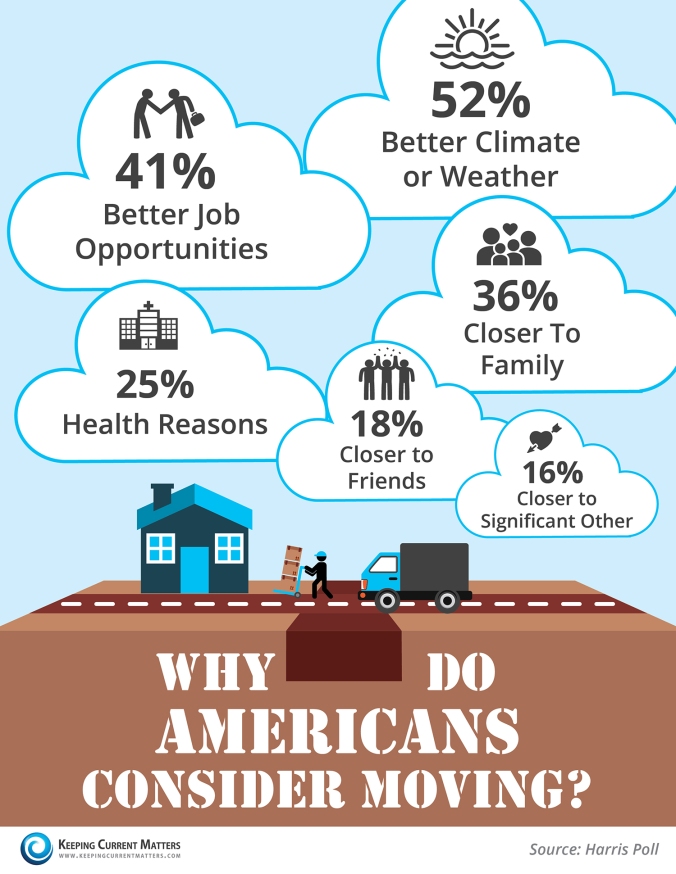

Top Six Reasons Why People Move

Share this:

FICO Score To Buy A House May Be Lower Than You Think!

Millennials: What FICO Score is Needed to Buy a Home?

In a recent article by the Wharton School of Business at the University of Pennsylvania, it was revealed that some Millennials are not looking to purchase a home simply because they don’t believe they can qualify for a mortgage.

The article quoted Jessica Lautz, the National Association of Realtors’ Managing Director of Survey Research, as saying that there is a significant population that does not think they will be approved for a mortgage and doesn’t even try. The article also quoted Fannie Mae CEO Tim Mayopoulos :

“I do think that there’s a sense out there in the marketplace among borrowers that credit may not be available, especially for people with lower credit scores.”

So what credit score is necessary?

A recent survey reported that two-thirds of the respondents believe they need a very good credit score to buy a home, with 45 percent thinking a “good credit score” is over 780.

In actuality, the FICO score on closed loans (as reported by Ellie Mae) is much lower and has been dropping over the last several months.

Bottom Line

Millennials who are considering a home purchase should get advice from a local real estate or mortgage professional now. They may be surprised how much the requirements for a mortgage have eased.

Share this:

Like A Virgin

![Buying A Home Can Be Scary... Until You Know the FACTS! [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/10/Mythbusters-KCM.jpg)

Some Highlights From Keeping Current Matters

- 36% of Americans think they need a 20% down payment to buy a home. 44% of Millennials who purchased a home this year have put down less than 10%.

- 71% of loan applications were approved last month

- The average credit score of approved loans was 723 in September (the lowest recorded score since Ellie Mae began tracking in August 2011).

Share this:

Rent vs Buy

Here is a great article from the Keeping Current in Real Estate Blog.

In the latest Rent vs. Buy Report from Trulia, they explained that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage throughout the 100 largest metro areas in the United States. The updated numbers actually show that the range is from an average of 16% in Honolulu (HI), all the way to 55% in Sarasota (FL), and 35% Nationwide!

The other interesting findings in the report include:

- Interest rates have remained low and even though home prices have appreciated around the country, they haven’t greatly outpaced rental appreciation. “In the past year, these two trends have made homeownership even more affordable compared with renting.”

- Some markets might tip in favor of renting if home prices increase at a greater rate than rents and if – as most economists expect – mortgage rates rise, due to the strengthening economy.

- Nationally, rates would have to rise to 10.6% for renting to be cheaper than buying – and rates haven’t been that high since 1989.

Bottom Line

Buying a home makes sense socially and financially. Rents are predicted to increase substantially in the next year, lock in your housing cost with a mortgage payment now.

Share this:

Home Loan Application

What you will need to have to make your home loan application

There are numerous home loans available today, including FHA, VA and Conventional. All of these loans will require you to fill out a loan application. This process is much easier if you are prepared. Here is a list of required items you are going to need:

1. Latest 2 paycheck stubs

2. Last 2 years W-2’s or 1099’s

3. If self-employed; last 2 years tax returns

4. Most recent bank statements (all your accounts for 2 months)

5. Loan and lease information on other real estate owned

6. Drivers license or other form of ID

Your lender may want more information and if they do, they will ask for it. Like the boy scouts, “Be prepared”, and you will have completed your loan application in no time!

Share this:

Buyer’s Closing Costs Explained

Here is a great video from WAHomeowners.com that explains the costs that occur when you buy a home.

Share this:

The Appraisal Process

When purchasing a property with a new loan, the lender will require the home to be appraised to determine fair market value, and that the sales price is warranted. A licensed appraiser will be assigned to complete the appraisal and will begin researching nearby houses that have sold in the last 6 months and are similar to the home being purchased in size, age, style, construction and amenities.

When purchasing a property with a new loan, the lender will require the home to be appraised to determine fair market value, and that the sales price is warranted. A licensed appraiser will be assigned to complete the appraisal and will begin researching nearby houses that have sold in the last 6 months and are similar to the home being purchased in size, age, style, construction and amenities.

The appraiser will visit the property and will take 30 minutes to an hour to look the property over. The appraiser will measure the home to determine square footage and draw out the floor plan, take photographs both inside and out and review the home’s overall condition, upgrades, and amenities.

The appraiser will provide the buyer’s lender an appraisal within a few days of visiting the home. If the appraiser has recommended repairs to the property, these repairs must be completed and re-inspected by the appraiser before the loan process can be completed.