What you will need to have to make your home loan application

There are numerous home loans available today, including FHA, VA and Conventional. All of these loans will require you to fill out a loan application. This process is much easier if you are prepared. Here is a list of required items you are going to need:

1. Latest 2 paycheck stubs

2. Last 2 years W-2’s or 1099’s

3. If self-employed; last 2 years tax returns

4. Most recent bank statements (all your accounts for 2 months)

5. Loan and lease information on other real estate owned

6. Drivers license or other form of ID

Your lender may want more information and if they do, they will ask for it. Like the boy scouts, “Be prepared”, and you will have completed your loan application in no time!

![Buying A Home Can Be Scary... Until You Know the FACTS! [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/10/Mythbusters-KCM.jpg)

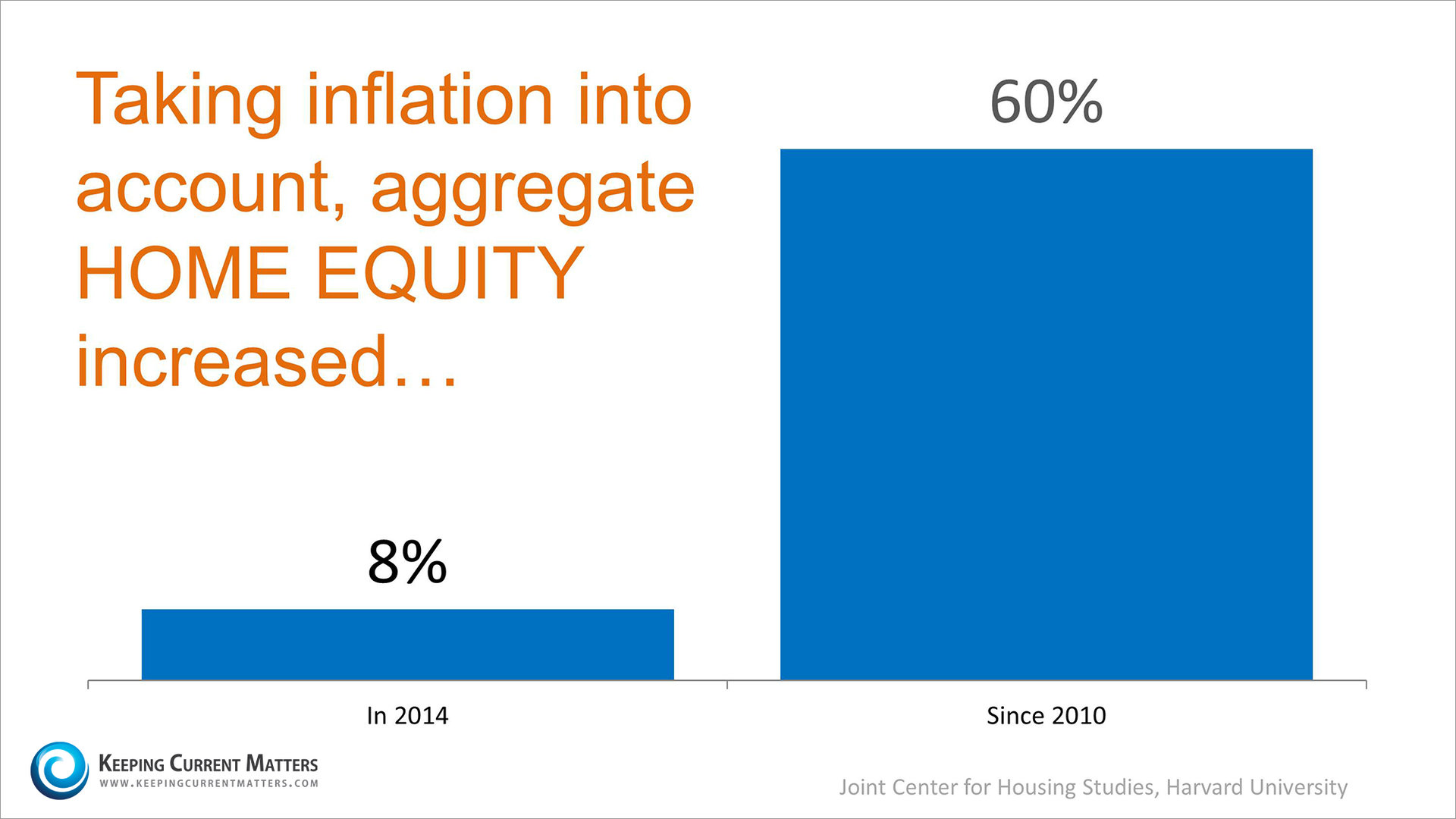

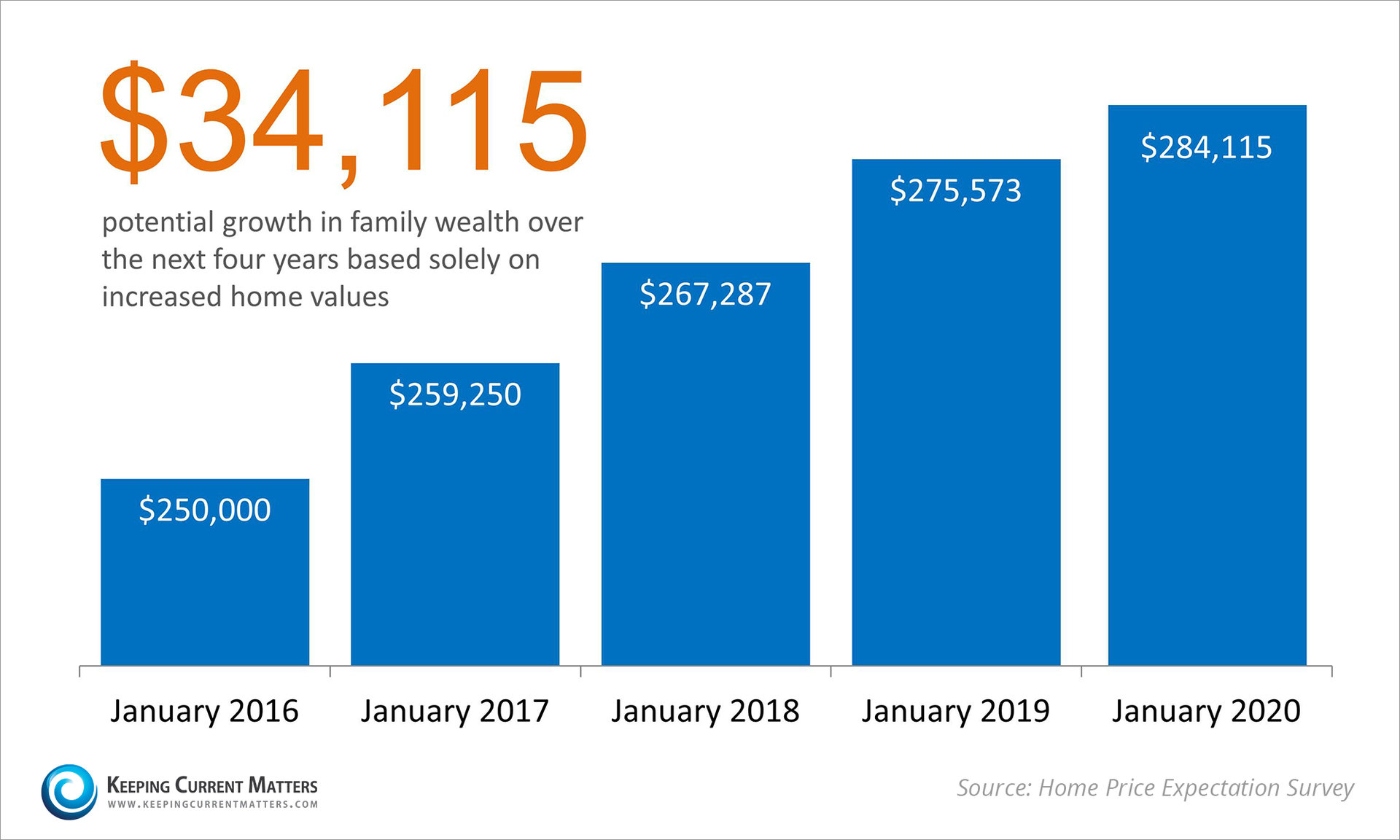

With residential real estate values rising quite substantially in most parts of the country over the last few years, many homeowners are seeing a major increase in their family’s wealth as equity continues to build in their house. A

With residential real estate values rising quite substantially in most parts of the country over the last few years, many homeowners are seeing a major increase in their family’s wealth as equity continues to build in their house. A

![Existing Home Sales Slow Amongst Tight Inventory [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/09/EHS-SEP.jpg)

Being “represented” by a REALTOR® means that you have an advocate who is putting themselves in your shoes. They will listen intently to you. They want as much information about your situation as possible so that they can best help you. They will do everything they can to earn your respect so that you will use them again in the future. Understanding our clients needs and wants is essential for success in this business.

Being “represented” by a REALTOR® means that you have an advocate who is putting themselves in your shoes. They will listen intently to you. They want as much information about your situation as possible so that they can best help you. They will do everything they can to earn your respect so that you will use them again in the future. Understanding our clients needs and wants is essential for success in this business.