| Keeping Current Matters recently published this great article on home buying.

CoreLogic’s latest Home Price Index reports that home prices have appreciated by 6.3% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 5.4% over the next year. The Home Price Expectation Survey polls a distinguished panel of over 100 economists, investment strategists, and housing market analysts. Their most recent report projects home values to appreciate by more than 3.2% a year for the next 5 years. The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have remained below 4%. Most experts predict that they will begin to rise over the next 12 months. The Mortgage Bankers Association, Freddie Mac & the National Association of Realtors are in unison projecting that rates will be up almost three-quarters of a percentage point by this time next year. An increase in rates will impact YOUR monthly mortgage payment. Your housing expense will be more a year from now if a mortgage is necessary to purchase your next home.

As a paper from the Joint Center for Housing Studies at Harvard University explains: “Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return. That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise. But what if they weren’t? Would you wait? Look at the actual reason you are buying and decide whether it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer or you just want to have control over renovations, maybe it is time to buy. If the right thing for you and your family is to purchase a home this year, buying sooner rather than later could lead to substantial savings.Bottom LineIf you are ready and willing to buy, find out if you are able to. Meet with a local real estate professional who can help you find your dream home |

home loan

With spring right around the corner, you may be wondering if you should wait to enter the housing market. Here are four great reasons to consider buying a home today instead of waiting.

With spring right around the corner, you may be wondering if you should wait to enter the housing market. Here are four great reasons to consider buying a home today instead of waiting.

What Do You Actually Need To Get A Mortgage

Another Great Article From: Keeping Current Matters Fannie Mae recently released their “What do consumers know about the Mortgage Qualification Criteria?” Study. The study revealed that Americans are misinformed about what is required to qualify for a mortgage when purchasing a home. Here are three takeaways:

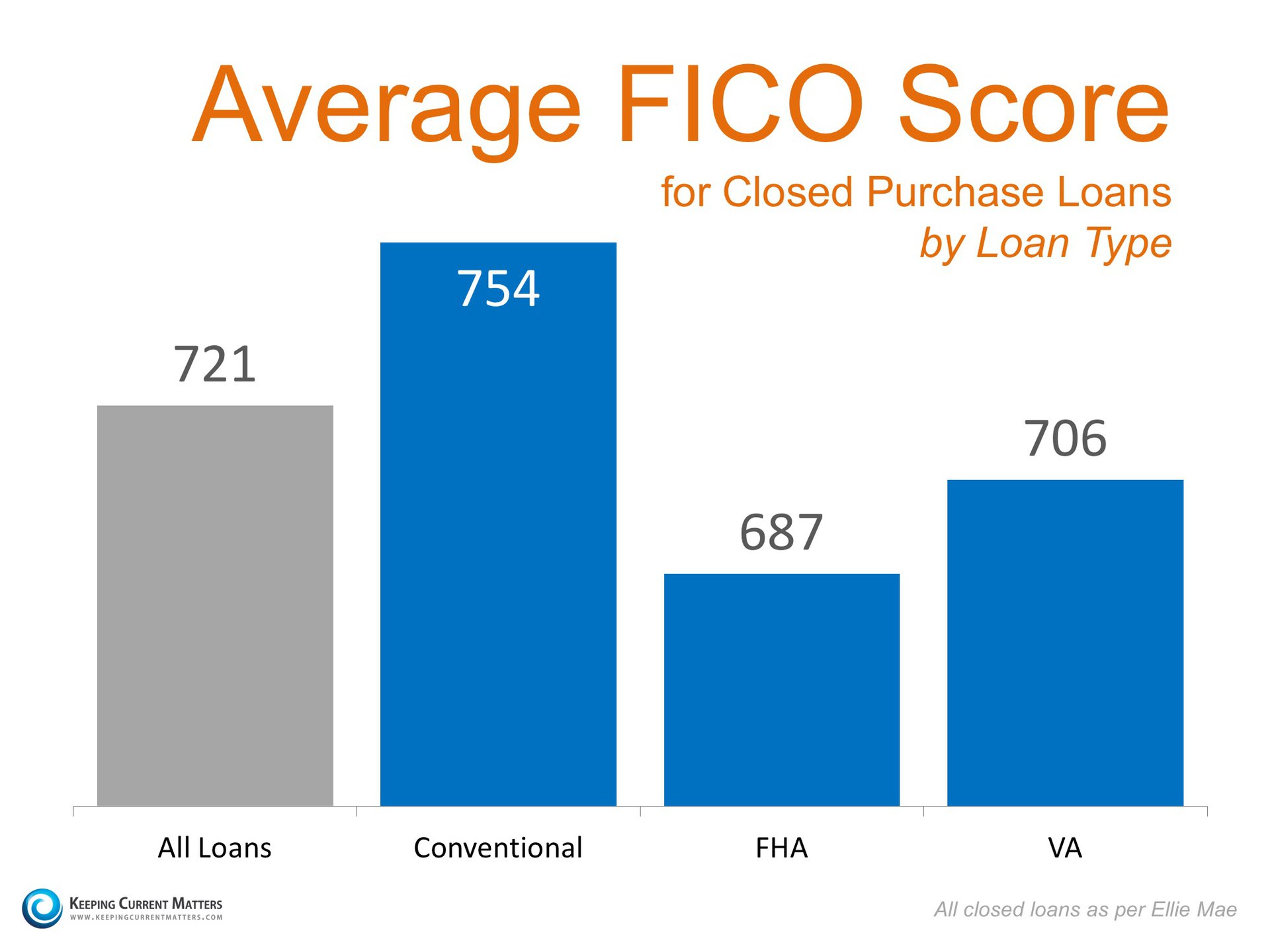

- 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO score is necessary

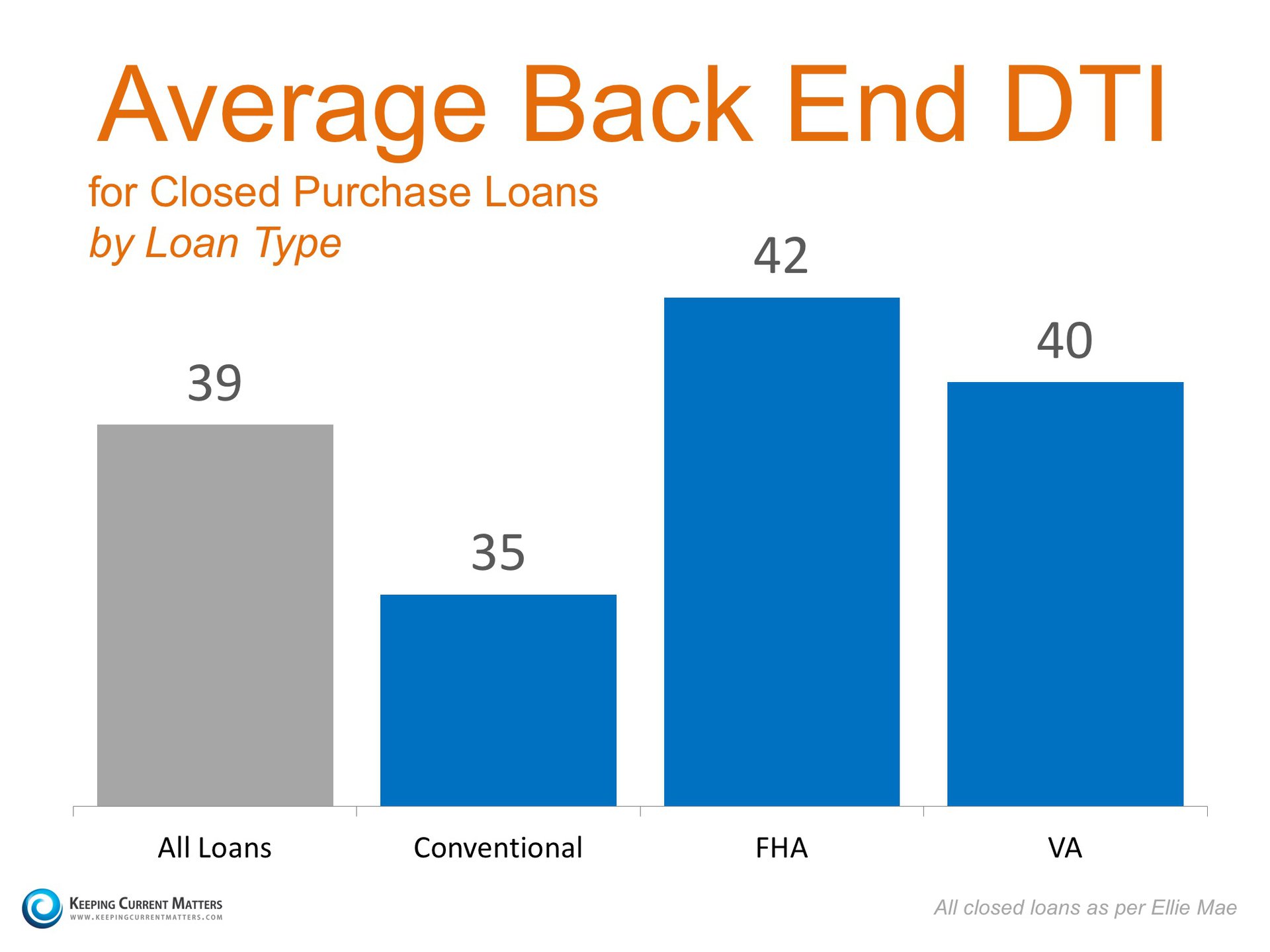

- 86% of Americans either don’t know (59%) or are misinformed (25%) about what an appropriate Back End Debt-to-Income (DTI) ratios is

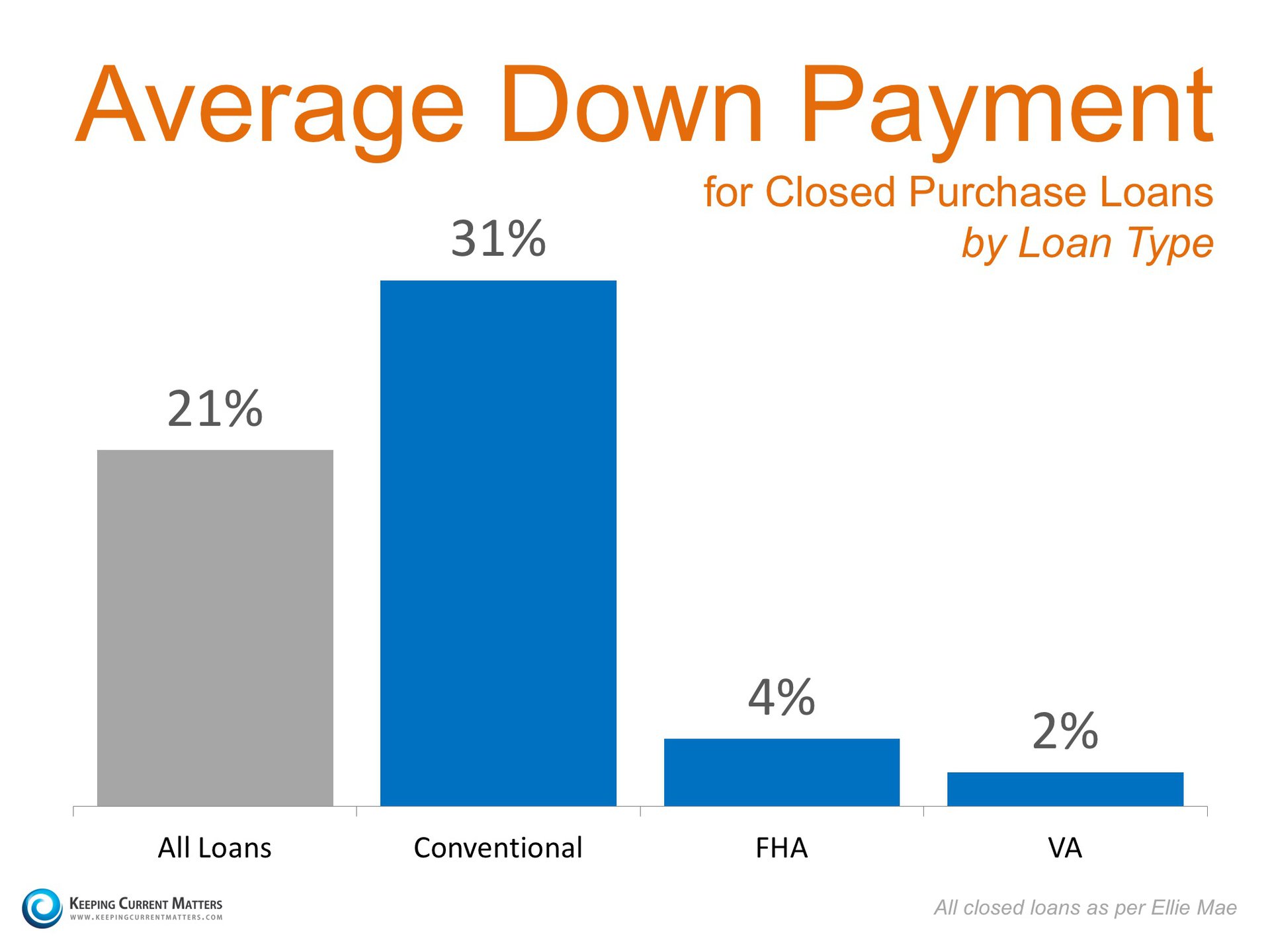

- 76% of Americans either don’t know (40%) or are misinformed (36%) about the minimum down payment required

To help correct these misunderstandings, let’s take a look at the latest Ellie Mae Origination Insight Report, which focuses on recently closed (approved) loans.

FICO SCORES

BACK END DTI

DOWN PAYMENTS

Bottom Line

Whether buying your first home or moving up to your dream home, knowing your options will definitely make the mortgage process easier. Your dream home may already be within your reach.

Share this:

Buy Now or Wait Until 2017

![Should I Buy Now Or Wait Until Next Year? [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2016/01/Cost-of-Waiting-KCM.jpg)

Some Highlights:

|

Share this:

Nine Steps To Buying A Home

Share this:

FICO Score To Buy A House May Be Lower Than You Think!

Millennials: What FICO Score is Needed to Buy a Home?

In a recent article by the Wharton School of Business at the University of Pennsylvania, it was revealed that some Millennials are not looking to purchase a home simply because they don’t believe they can qualify for a mortgage.

The article quoted Jessica Lautz, the National Association of Realtors’ Managing Director of Survey Research, as saying that there is a significant population that does not think they will be approved for a mortgage and doesn’t even try. The article also quoted Fannie Mae CEO Tim Mayopoulos :

“I do think that there’s a sense out there in the marketplace among borrowers that credit may not be available, especially for people with lower credit scores.”

So what credit score is necessary?

A recent survey reported that two-thirds of the respondents believe they need a very good credit score to buy a home, with 45 percent thinking a “good credit score” is over 780.

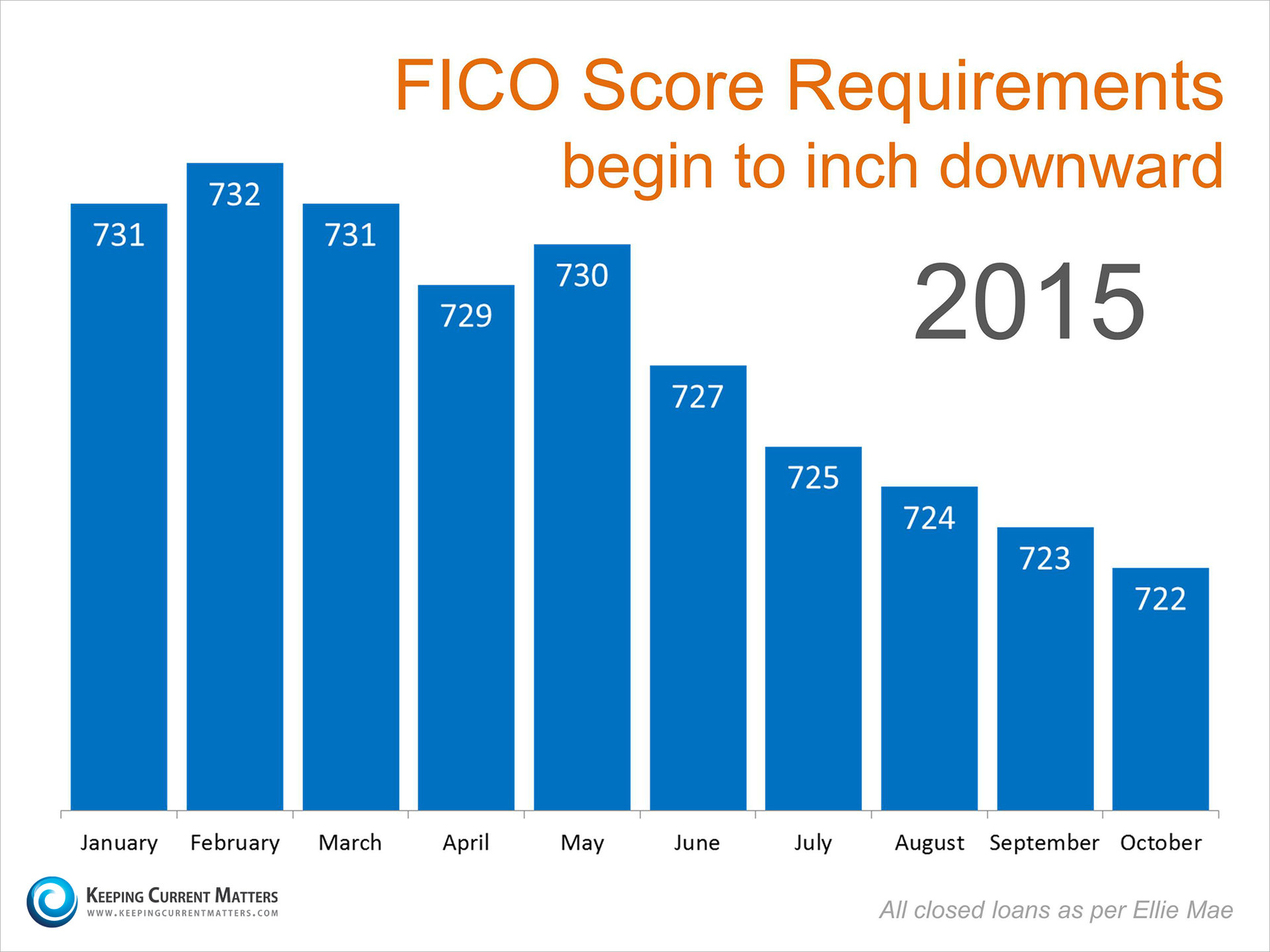

In actuality, the FICO score on closed loans (as reported by Ellie Mae) is much lower and has been dropping over the last several months.

Bottom Line

Millennials who are considering a home purchase should get advice from a local real estate or mortgage professional now. They may be surprised how much the requirements for a mortgage have eased.

Share this:

Like A Virgin

![Buying A Home Can Be Scary... Until You Know the FACTS! [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/10/Mythbusters-KCM.jpg)

Some Highlights From Keeping Current Matters

- 36% of Americans think they need a 20% down payment to buy a home. 44% of Millennials who purchased a home this year have put down less than 10%.

- 71% of loan applications were approved last month

- The average credit score of approved loans was 723 in September (the lowest recorded score since Ellie Mae began tracking in August 2011).

Share this:

Home Loan Application

What you will need to have to make your home loan application

There are numerous home loans available today, including FHA, VA and Conventional. All of these loans will require you to fill out a loan application. This process is much easier if you are prepared. Here is a list of required items you are going to need:

1. Latest 2 paycheck stubs

2. Last 2 years W-2’s or 1099’s

3. If self-employed; last 2 years tax returns

4. Most recent bank statements (all your accounts for 2 months)

5. Loan and lease information on other real estate owned

6. Drivers license or other form of ID

Your lender may want more information and if they do, they will ask for it. Like the boy scouts, “Be prepared”, and you will have completed your loan application in no time!

Share this:

First Time HomeBuyer Pitfalls

Share this:

Get The Best Home Loan For You

After completing steps 1 and 2 in the loan process it is NOW time to SHOP FOR YOUR LOAN. You will need to know and factor in these 5 specifics:

1. The price of the home

2. Your down payment amount, resulting in the amount you will finance.

3. The interest rate and any points charged to originate the loan.

4. The term of your loan: 15 year or 30 year.

5. Type of loan: fixed vs variable rate, conventional or FHA financing, there are many loans to choose from.

To shop for the best financing for you, do your homework. Research these items so you understand what your mortgage lender is talking about. Now, go and talk to 2 or 3 lenders. Knowing these specifics will help you compare loans, so you can choose the loan and lender that will be the best deal for you.

Your Home Loan Application

There are numerous home loans available today, including FHA, VA and Conventional. All of these loans will require you to fill out a loan application. This process is much easier if you are prepared. Here is a list of required items you are going to need:

There are numerous home loans available today, including FHA, VA and Conventional. All of these loans will require you to fill out a loan application. This process is much easier if you are prepared. Here is a list of required items you are going to need:

1. Latest 2 paycheck stubs

2. Last 2 years W-2’s or 1099’s

3. If self-employed; last 2 years tax returns

4. Most recent bank statements (all your accounts for 2 months)

5. Loan and lease information on other real estate owned

6. Drivers license or other form of ID

Your lender may want more information and if they do, they will ask for it. Like the Boy Scouts, “Be prepared”, and you will have completed your loan application in no time.