As a member of the National Association of REALTORS, I receive news about Real Estate. This article clarifies mortgage interest deduction on a home equity loan.

The Internal Revenue Service (IRS) has issued a news release(link is external) clarifying that in many cases, interest paid on home equity loans remains deductible under the new tax reform law. Many questions have arisen on this issue, as many media reports on the new tax law indicated that as of 2018, interest is no longer deductible on home equity loans. The IRS stated that “despite newly-enacted restrictions on home mortgages, taxpayers can often still deduct interest on a home equity loan, home equity line of credit (HELOC) or second mortgage, regardless of how the loan is labelled.” The key factor is that the proceeds of such loans must be used to buy, build, or substantially improve the taxpayer’s home that secures the loan. Interest on a home equity or other loan used for personal living expenses (e.g. paying off credit card debt, education, or vacation expenses) would not be deductible.

According to a Merrill Lynch

According to a Merrill Lynch

With spring right around the corner, you may be wondering if you should wait to enter the housing market. Here are four great reasons to consider buying a home today instead of waiting.

With spring right around the corner, you may be wondering if you should wait to enter the housing market. Here are four great reasons to consider buying a home today instead of waiting.

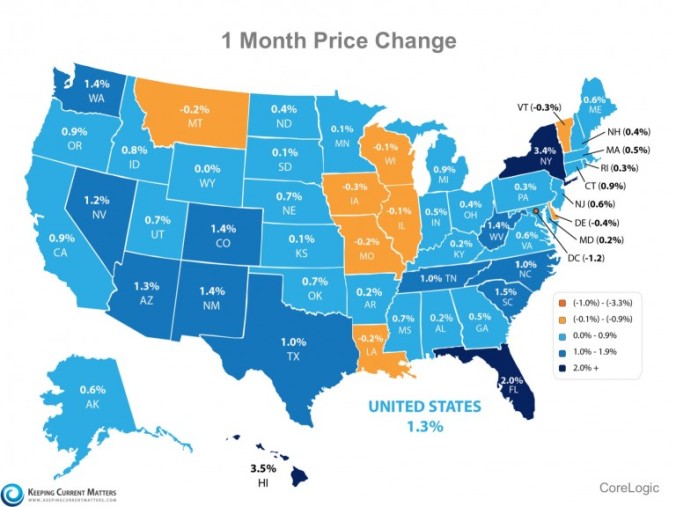

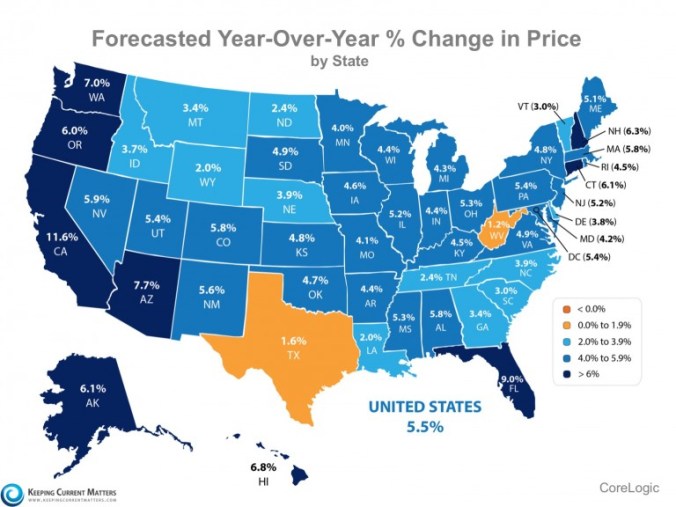

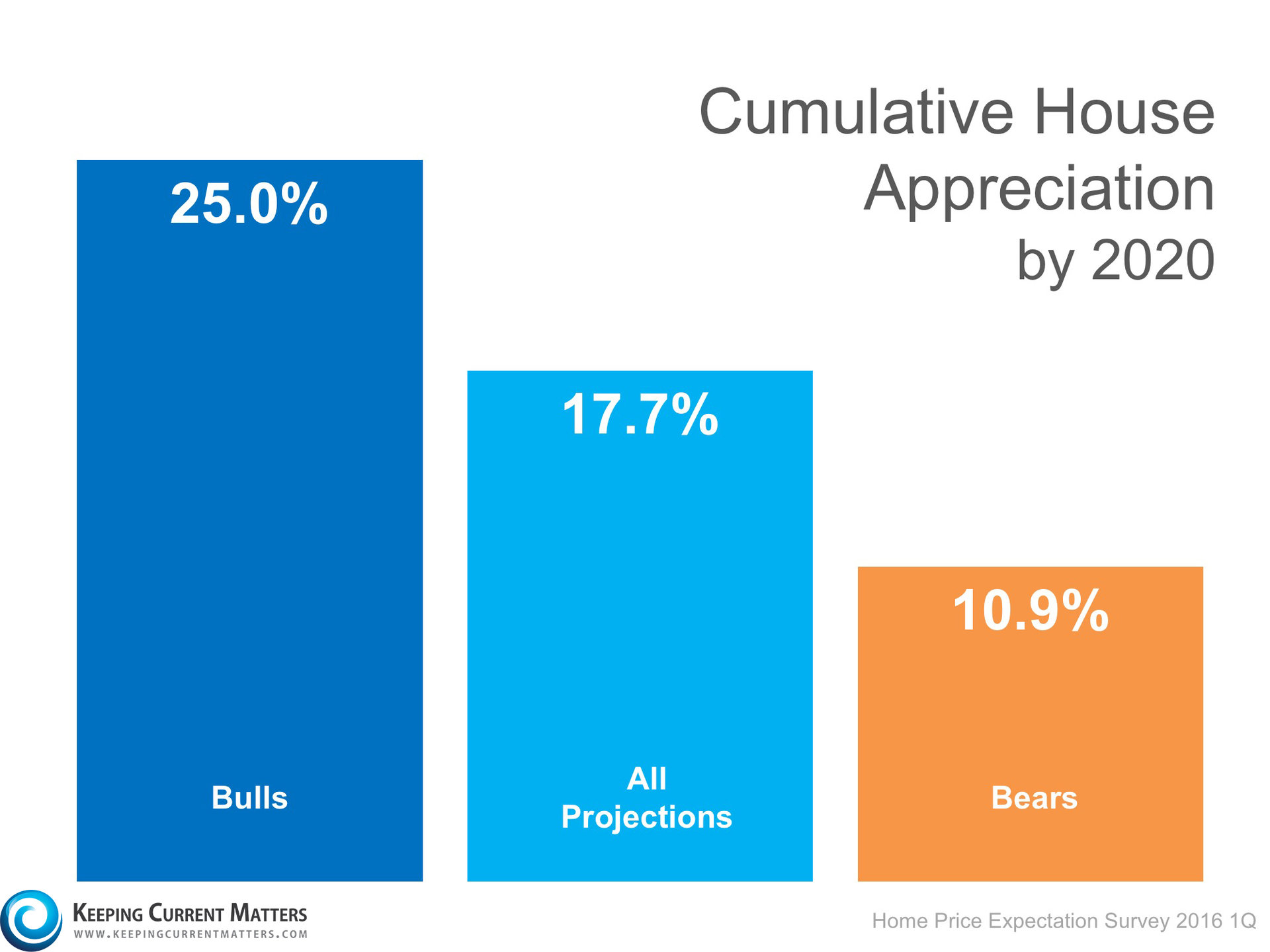

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the

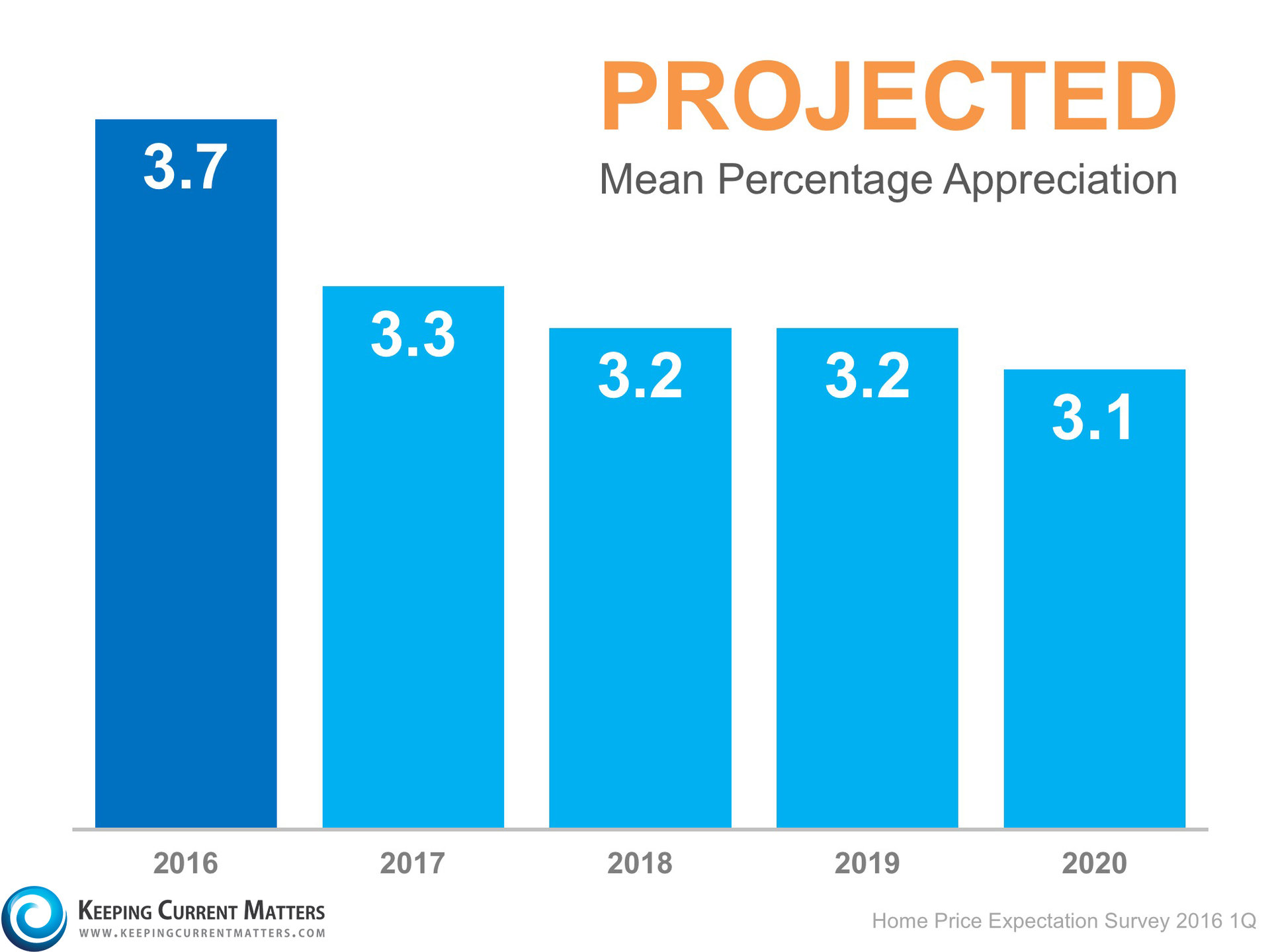

Fannie Mae recently released their

Fannie Mae recently released their